Global economic conditions in 2025 present a complex landscape for investors, marked by shifting risks and divergent regional trajectories. With geopolitical instability, trade policy changes, and monetary policy adjustments reshaping markets, adaptability and scenario-based planning have become critical tools for navigating uncertainty.

Key Economic Risks and Trends

Geopolitical instability and trade policy shifts now rank equally as top disruptors to global growth, according to McKinsey’s March 2025 survey13. Over 68% of executives now view a consumer sentiment-driven recession as the most likely near-term scenario, up sharply from late 20243. These risks coincide with uneven monetary policy responses:

- Mexico and the ECB have implemented rate cuts (9.0% and -25 bps respectively)3

- Russia and Brazil continue tightening to combat inflation3

- The IMF projects global growth at 3.3% for 2025-2026, with advanced economies slowing to 1.8% while emerging markets maintain 4.2% expansion5

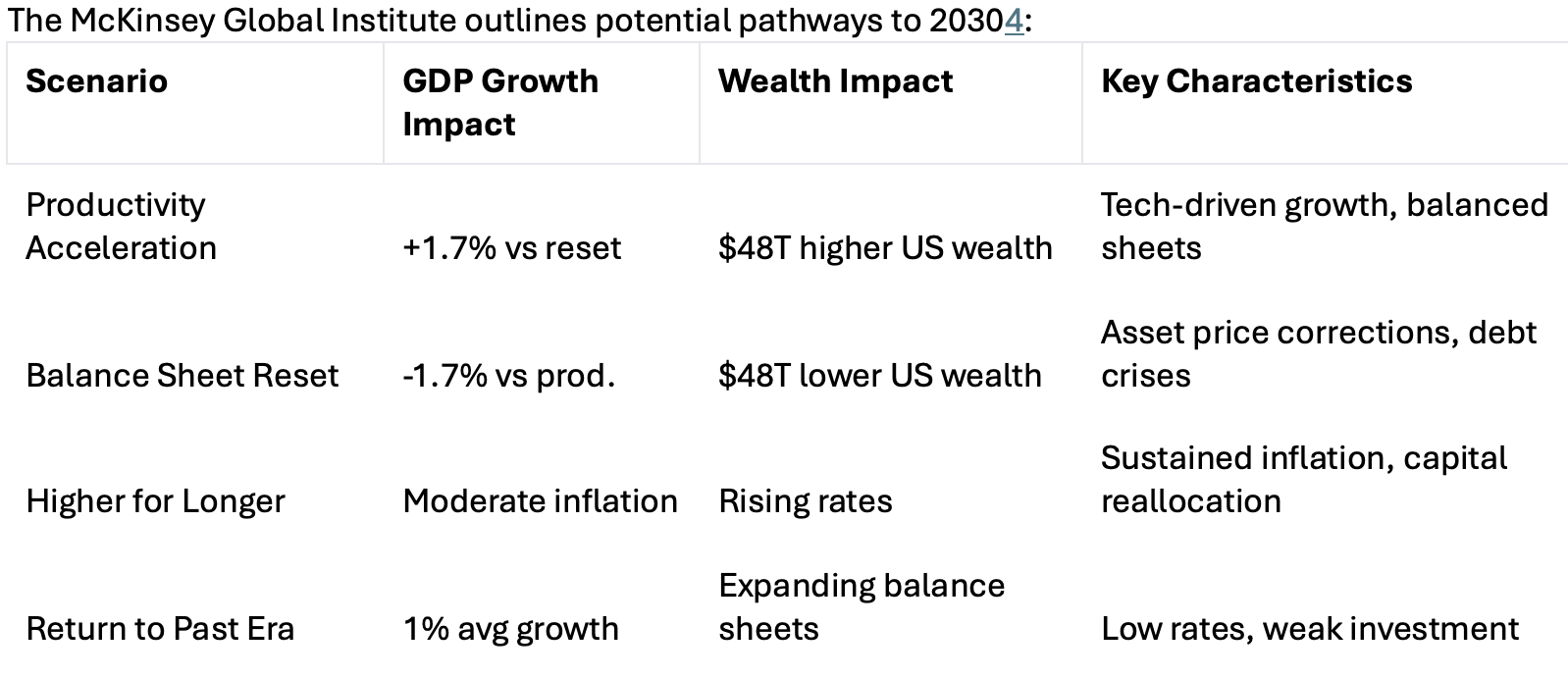

Four Long-Term Scenarios

The McKinsey Global Institute outlines potential pathways to 20304:

Strategic Imperatives for Investors

- Diversify across economic scenarios: Allocate assets to hedge against both inflationary (commodities, TIPS) and deflationary (long-term bonds, utilities) outcomes45.

- Monitor central bank pivot points: Track real interest rates in emerging markets (-1.4% avg) versus developed economies (+0.8% avg)35.

- Prioritize productivity-linked sectors: McKinsey estimates productivity gains could add $15T annually to global GDP by 2030 in optimal conditions4.

- Reassess emerging market exposure: While IMF projects 4.2% EM growth, focus on nations with <60% debt/GDP ratios and diversified export profiles5.

Disclosure: this article is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities. The views and opinions expressed are based on publicly available information and third-party sources, including but not limited to the World Economic Forum, J.P. Morgan Private Bank, the International Monetary Fund (IMF), LGT Wealth Management, WRISE, S&P Global, and MSCI. While reasonable efforts have been made to ensure the accuracy of the information presented, no representation or warranty is made as to its completeness or accuracy. Past performance is not indicative of future results. Investing involves risks, including the possible loss of principal. Readers should not rely solely on this article for investment decisions and are encouraged to consult with a qualified financial advisor or other professional before making any investment or financial decisions. The information herein may be subject to change without notice and may not reflect the most current regulatory or market developments. This analysis incorporates third-party research from McKinsey & Company and the International Monetary Fund. Past performance does not guarantee future results. Investors should consult financial advisors regarding specific portfolio decisions.

Sources

- https://www.weforum.org/publications/global-risks-report-2025/in-full/global-risks-2025-a-world-of-growing-divisions-c943fe3ba0/

- https://reports.weforum.org/docs/WEF_Global_Risks_Report_2025.pdf

- https://www.weforum.org/stories/2024/12/global-trade-geopolitics-uncertainty-economic-policy/

- https://www.weforum.org/stories/2025/04/long-term-economic-trends-growth-economy/

- https://www.weforum.org/stories/2025/01/global-financial-system-fragmentation/

- https://www.weforum.org/publications/global-risks-report-2024/digest/

- https://www.weforum.org/stories/2025/02/how-to-enhance-geopolitical-risk-assessment-using-combined-strategy/

- https://www.weforum.org/publications/global-risks-report-2024/

- https://www.blackrock.com/corporate/insights/blackrock-investment-institute/interactive-charts/geopolitical-risk-dashboard

- https://x.com/wef

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119