%20Withdrawals.png)

By Gary Lendermon

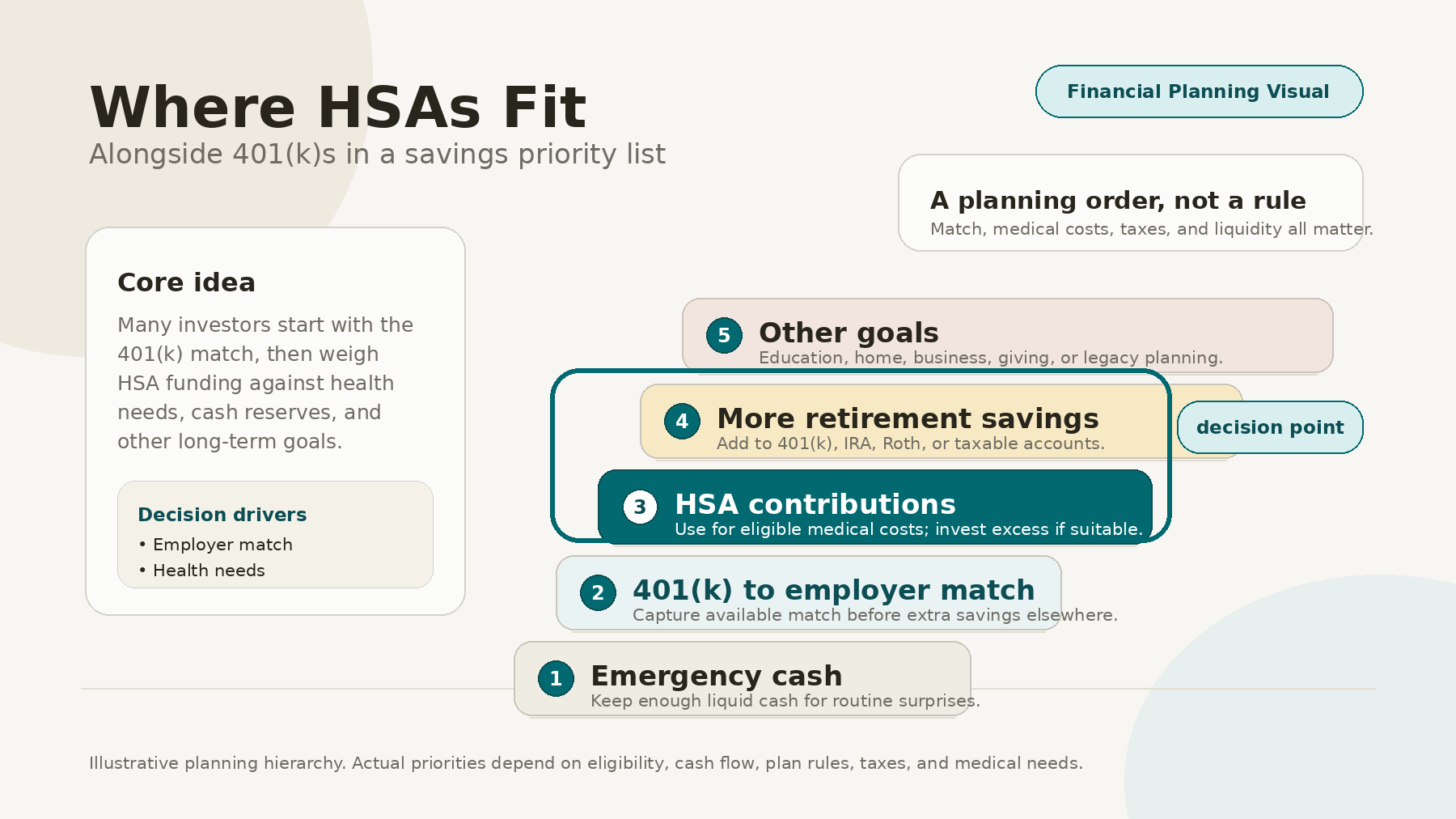

Are you thinking about dipping into your 401(k) before retirement? It might seem like a quick fix for financial needs, but let's discuss the actual cost. There are penalties, taxes, and missed investment growth to consider. Understanding these factors is crucial for making informed decisions about your retirement savings.

When you take money out of your 401(k) before age 59½, the IRS slaps you with a 10% early withdrawal penalty. On top of that, the withdrawn amount is treated as ordinary income, so get ready to owe federal and possibly state income taxes.

These penalties and taxes can eat up a significant chunk of your money. For example, if you pull out $50,000 and are in the 24% federal tax bracket, you might be left with only $33,000 after taxes and penalties —a 34% loss of your savings.

But the real kicker is the missed opportunity for investment growth. Your 401(k) is designed to grow over time through contributions and compounding interest. When you take money out early, you're kissing that growth goodbye.

For instance, if you withdraw $50,000 at age 35 instead of letting it grow, you could be waving goodbye to the potential growth of around $140,000 by the time you hit 65.

This can seriously mess with your retirement plans. Most financial experts advise saving at least 10 to 12 times your annual income by retirement. Even taking out a small portion of your 401(k) balance could make reaching this goal challenging and even force you to delay your retirement or adjust your lifestyle.

And once you take the money out, there's no putting it back. Annual contribution limits make it hard to catch up if you've taken out a substantial amount.

Before you make any moves, it's worth exploring other options, like borrowing from your 401(k) if your plan allows it or considering a hardship withdrawal if you're facing specific circumstances like medical emergencies or buying a home. If you're leaving your job, rolling your 401(k) to an IRA could also be wise.

In short, cashing out your 401(k) can be costly, with immediate and long-term financial consequences. It can seriously dent your retirement savings and make reaching your long-term financial goals harder. Before you take any steps, it's vital to consider your options and consult a DWAM financial advisor for a clearer picture.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Duncan Williams Asset Management (DWAM) does not guarantee the information's accuracy, completeness, or timeliness. The views expressed are those of the author and may not reflect the official policy or position of DWAM.

All investments carry risk, including loss of principal. Any references to specific financial products or services do not constitute an endorsement or recommendation by DWAM. Individuals should consult their financial, tax, or legal advisors before deciding on 401(k) or other investment accounts. Past performance is not indicative of future results.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119